FASBs New standard for leases

In February 2016, the Financial Accounting Standards Board (FASB) finalized its new standard for leases. This project began around 2006 as a joint project with the International Accounting Standards Board (IASB) to create an accounting standard that provides a more faithful representation of leasing transactions in financial reports. The most significant change coming out of this project is that most leases, including operating leases, will be recognized on the balance sheet as a right-of-use (ROU) asset and a lease obligation (liability). In this article, we will explore the various changes in this accounting standard.

Lease Classification

The new definition of a lease was modified only slightly and, in practice, will not change how we define most lease contracts. Lessees may need to carefully consider whether contracts include non-lease components. For example, a copier lease may include a maintenance agreement that is included in the total lease payment. Under the new standard, the non-lease component should be accounted for separately from the lease; however, a lessee can make an accounting policy election to treat all non-lease components as part of the lease contract, which will simplify the accounting but may inflate the recognized right-of-use asset and lease obligation. Lease terms will include the following elements:

- Noncancelable lease period(s)

- Periods covered by an option to extend that the lessee is reasonably certain to exercise (The term “reasonably certain” is intended to be a relatively high threshold in the standard)

- Periods covered by an option to terminate that the lessee is reasonably certain not to exercise

- Periods covered by an option to extend (or option to terminate) controlled by the lessor

Similar to current accounting rules, lessees (and lessors) will classify leases as operating or finance leases based on five criteria:

- The lease transfers ownership of the underlying asset to the lessee.

- The lease grants the lessee an option to purchase the underlying asset that the lessee is reasonably certain to exercise.

- The lease term is for the major part of the remaining economic life of the asset.

- The present value of the lease payments and any residual value guarantee by the lessee equals or exceeds substantially all of the fair value of the asset.

- The underlying asset is so specialized it has no alternative use to the lessor.

These criteria are intended to be principle based, although current rules may be used as guidelines. For instance, if the present value of the lease payments is approximately 90% of the fair value of the underlying asset, this most likely indicates the “substantially all” threshold has been met.

If the lease meets any of these five criteria, the lessee will classify the lease as a finance lease. If not, the lessee will classify it as an operating lease.

Accounting Change

For both operating and finance leases, the lessee will recognize a right-of-use asset and a lease obligation for the present value of payments paid over the lease term. The right-of-use asset may be adjusted for initial direct costs, prepayments, and/or lease incentives. Subsequently, the lease obligation for both types of leases will be reduced for the principal component of each lease payment.

Amortization of the right-of-use asset will be different depending on the type of lease. For finance leases, the right-of-use asset will be amortized consistent with other fixed assets. Generally, the asset will be amortized on a straight-line basis over the shorter of the lease term or the useful life of the asset.

For operating leases, the right-of-use asset will be amortized in such a way that the amount of lease expense recognized is usually the same from period to period. In other words, the reduction of the right-of-use asset will be whatever is necessary to recognize a straight-line lease expense in the income statement.

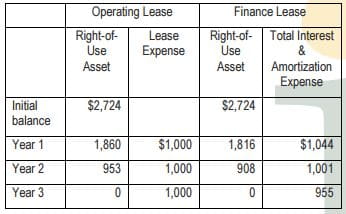

Here is a simple example of the differences in accounting for operating and finance leases. Let’s assume the following:

- Lease contract requires annual payments of $1,000 for three years.

- Present value of lease payments is $2,724.

- There are no initial direct costs, prepayments, or lease incentives.

In either case, the lessee will recognize a right-of-use asset and a lease obligation of $2,724. If this lease is considered a finance lease, the lessee will make the following entry at the end of year one when the first lease payment is made:

- Dr Lease obligation $864

- Dr Interest expense 136

- Dr Amortization expense 908

- Cr Cash $1,000

- Cr Right-of-use asset 908

If this lease is considered an operating lease, the lessee will make the following entry after the first lease payment:

- Dr Lease obligation $864

- Dr Lease expense 1,000

- Cr Cash $1,000

- Cr Right-of-use asset 864

The accounting for the lease obligation is identical for either type of lease. The following table demonstrates the differences in the subsequent measurement of the right-of-use asset and expense:

Changes for Lessors

The impact of this standard on lessors is relatively minor. Leveraged leases, one of the four types of leases under current accounting standards, will go away. Under the new standard, leases will be classified as sales-type if they meet one of the five lease classification criteria or as direct finance or operating if they don’t meet any of the lease classification criteria. However, leveraged leases in existence when the new standard is adopted will be grandfathered in and continue to be accounted for using the existing leveraged lease rules. In addition, the special rules for real estate leases will be removed in the new accounting standard.

Other Changes

The new lease standard also provides new guidance in a number of other areas, including sale-leaseback transactions, related-party leasing arrangements, lease modifications, and financial statement presentation and disclosures. For more information on any of these changes, please contact your Wipfli relationship executive.

Effective Date and Transition

ASU No. 2016-02 will be effective for public companies, which include public business entities and certain other entities that file with the SEC, for fiscal years beginning after December 15, 2018, including interim periods within those fiscal years. For other entities, the standard is effective for fiscal years beginning after December 15, 2021, and interim periods after that year. Early adoption of this standard is permitted. Upon adoption, existing leases will be recognized as right-of-use assets and lease obligations as of the beginning of the earliest financial statement presented. For institutions that only prepare call reports, it appears this would be as of January 1, 2022.

Final Thoughts

The new standard for leases may or may not have a significant impact on your institution’s financial statements depending on how significant your leasing arrangements are. It is also important that your loan staff understand how this standard will impact borrower’s financial statements. If you have any questions regarding this new standard, please contact Brett Schwantes or your Wipfli relationship executive.