ASC 606: The Devil Is in the Details – Six Key Considerations to Take Away From the New Revenue Recognition Standard

In May 2014, the Financial Accounting Standards Board (FASB) completed its revenue recognition project by issuing Accounting Standards Update (ASU) No. 2014-09, Revenue from Contracts with Customers, which can be found in the Accounting Standards Codification (ASC) Topic 606.

This article will cover six topics within ASC 606 that will likely impact your organization.

1. Reviewing existing contracts and the importance of understanding termination clauses

ASC 606 states that contracts must meet the following criteria to recognize revenue:

- The contract must have commercial substance.

- The parties have approved the contract and are committed to their respective obligations.

- Each party’s rights regarding the services provided are known.

- The payment terms for the services are known.

- It is probable that the entity will collect the amount of consideration to which the organization will be entitled.

ASC 606 states that a contract does not exist if each party to the contract has the unilateral enforceable right to terminate without compensating the other party. If a contract allows each party to terminate the contract without significant penalty (i.e., recover cost plus a markup), the organization must wait to record revenue until the following criteria are met:

- The entity has no remaining obligations to transfer goods or services to the customer, the entity has received substantially all payments (“consideration”) from the customer, and the amount received is nonrefundable.

- The contract has been terminated, and the amount received from the customer is nonrefundable.

- The entity has transferred control of the goods or services for which payment has been received, and the entity has no obligation under the contract to transfer additional goods or services. The amount of payment received from the customer is nonrefundable.

Organizations that have unilateral termination clauses will delay the recognition of revenue under ASC 606.

Takeaway #1: Many organizations have a contract review process in place. This process often involves multiple departments and, in some instances, external parties (e.g., finance department, legal counsel, materials management, sales representatives, etc.). All parties need to understand the impact of language within existing contracts, like termination clauses, and the effect this language will have on revenue recognition under ASC 606.

2. Identifying separate performance obligations

The second step in the revenue recognition five-step process is to identify the separate performance obligations. When determining the number of performance obligations in a contract, the organization should view the contract from the customer’s perspective and consider what goods or services the customer ultimately expects to receive as a result of the contract. ASC 606 states that if the organization can answer yes to both of the following questions, it is likely the contract contains more than one performance obligation:

- Are the goods or services capable of being sold separately?

- Upon receiving the goods or services, would the customer receive the economic benefits without needing other goods or services provided in the contract?

At first glance, it would appear that many contracts could be interpreted to have more than one separate performance obligation. Like many other accounting standards, ASC 606 has some exceptions. It states that two or more promises to transfer goods or services to a customer are not separately identifiable and should be viewed as one performance obligation if any of the following factors are met:

- There is a significant service of integrating goods or services together into a bundle of goods or services that the customer has contracted (e.g., customer expects a general contractor to construct a building in its entirety, even though the general contractor has to complete steps and tasks to construct the building).

- One or more of the goods or services significantly modify or customize other goods or services promised within the contract (e.g., engraving).

- The goods or services are highly interdependent or are each of the goods or services significantly affected by one or more of the other goods in the contract (e.g., the customer purchases highly specialized equipment parts that are used together to run the customer’s machinery; without all the equipment parts, the customer’s machinery will not operate properly).

Organizations will need to consider all facts and circumstances applicable to the contract when making a determination on the number of separate performance obligations within a contract.

Another issue relates to contracts with customer options to acquire additional goods or services for free or at a discount. ASC 606 states that if the customer’s option to acquire additional goods or services is at a price significantly below the standalone selling price, and if the customer receives the purchase option only by entering into the contract, then a separate performance obligation exists. The discount offered needs to be unique to the customer in the sense that the general public or other customers are not offered this same discount. For some industries it is common to offer discounts for early payment or discounts if a certain amount of goods are purchased within a period of time. These discounts are typically standard within the industry and do not provide the customer a significant right to purchase additional goods or services substantially below market rates.

Why is determining the various performance obligations important? Not all performance obligations in a contract will be recorded in revenue at the same time. Some performance obligations will be recognized in revenue at a point in time, and others will be recognized over time.

Takeaway #2: In many instances, identifying the number of performance obligations in a contract is not simple. The key to identifying the various performance obligations is to view the contract from the customer’s perspective. If promised goods or services are not distinct, ASC 606 states the entity may account for all the goods or services promised in a contract as a single performance obligation. Organizations should evaluate current contracts to understand the various performance obligations within a contract and determine the impact of how and when those performance obligations will be recognized under ASC 606.

3. Determining the transaction price: A two-step process

ASC 606 defines the transaction price as the amount of consideration an entity expects to be entitled to in exchange for transferring promised goods or services to a customer. In simpler terms, the transaction price is ultimately the amount the organization records as revenue for the services provided to a customer, net of all discounts, rebates, and refunds. The transaction price includes the effects of two factors: (1) variable consideration, which can be either explicit or implicit price concessions (i.e., discounts, rebates, refunds, credits, etc.), and (2) the consideration of a constraint. For the purpose of determining the transaction price, an entity shall assume that the goods or services will be transferred to the customer as promised in accordance with the existing contract and that the contract will not be cancelled, renewed, or modified.

ASC 606 states an organization shall estimate the amount of variable consideration using either of the following two methods, depending on which method better predicts the amount of revenue the organization will record from a particular contract.

- The expected value method. This is the sum or probability-weighted amounts in a range of possible outcomes. This method may be appropriate if the organization has a large number of contracts with similar characteristics.

- The most likely amount. The most likely amount is the single most likely in a range of possible outcomes. For contracts with one probable outcome (i.e., often considered greater than 75%-80% likely), it may make sense to use the most likely amount. An organization may use the most likely amount for contracts with only two possible outcomes (e.g., achieves a performance bonus or not).

ASC 606 requires an organization to consider the likelihood that a significant amount of the revenue recorded in the current period will not be adjusted up or down in future periods. The following are factors an organization should consider when evaluating the potential for a revenue adjustment in future periods:

- The amount the organization expects to receive is highly susceptible to factors outside the organization’s influence (e.g.., weather conditions, judgement or action of third parties like the government, high risk of obsolescence of the promised goods or services like software or electronics).

- The amount the organization expects to receive will not be resolved for a long period of time.

- The contract contains a large number and a broad range of possible outcomes.

- The organization does not have historical information from similar contracts to estimate probable outcomes.

Takeaway #3: Since the guidance for determining the transaction price within ASC 606’s principles-based standard is generic, organizations will need to use significant judgements when estimating the amount of revenue to record for each contract. Organizations will need to develop a robust policy to document the methods, inputs, and assumptions used to record revenue for their contracts. Organizations may be able to evaluate multiple contracts together if the contracts have similar characteristics, terms, and conditions as one portfolio of contracts. However, to view multiple contracts as a portfolio, organizations must be able to support that the financial outcome of the portfolio of contracts would not have differed materially had each contract been viewed and recorded separately.

4. Allocating the transaction price to the performance obligation(s)

The objective of allocating the transaction price to each performance obligation is to assign a value to the consideration that an organization would expect to be entitled to receive from a customer for the underlying promised good or service. The most basic method to accomplish this task is to assign the price by using a relative standalone price for each performance obligation (assuming it can be sold separately to similar customers). If that method is not practical or observable, ASC 606 allows for the organization to make a reasonable estimation of that price. Given that ASC 606 puts the burden on the entity to detail its estimation approach, it will be important for entities to consider a larger range of evidence (market conditions, entity-specific factors, etc.) and to document those methods in order to apply them in a consistent manner.

Since this process will involve more art than science and therefore significant judgment, ASC 606 guides the preparer toward three primary estimation approaches: (1) adjusted market assessment, (2) expected cost plus margin, and (3) residual. Entities are not limited to these approaches, however, and any method that is consistent with the concepts of standalone price and maximizing observable inputs—and is repeatable and consistently applied—is permitted.

Easy enough? As with all things that seem too good to be true, there are two exceptions to these general rules:

- Allocation of variable consideration (such as contingent bonuses or price increases based on inflation indices). Variable amounts can be allocated entirely to a distinct performance obligation if the following criteria are met:

- The variable consideration can be attributed specifically to a performance obligation, and

- Allocation of the variable amount is consistent with the allocation objective in ASC 606-10-32-28.

- Discounts allocation

- This most often applies to bundled goods and services. If a discount is not related to all of the goods and services, the discount should be applied to only those goods or services related to the discount.

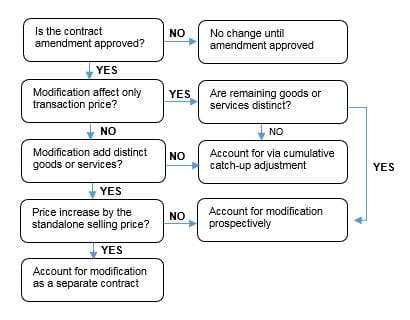

Contract Modifications

One of the more confusing new concepts in the ASC 606 framework is the notion of contract modifications. These are likely to be confused with the definition of performance obligations as a result of the broad factors involved in a contract modification. Accounting for contract modifications depends on several factors, as illustrated in the following table:

Takeaway #4: Document, document, document! It will be crucial for organizations to have a well-documented pricing methodology, including the significant judgements made, to support the transaction price assigned to each performance obligation. In addition, contract modifications are inevitable. It is important for organizations to understand how contract modifications will impact the recognition of revenue from contracts under ASC 606.

5. Point in time vs. over time

The general rule of thumb is that revenues must be recognized over time if any of the following conditions are true:

- The customer simultaneously receives and consumes the benefits.

- The seller’s performance creates or enhances an asset that the customer controls.

- The seller’s performance does not create an asset with an alternative use to the seller, and the seller has an enforceable right to payment for performance completed to date.

If none of those conditions apply, revenue should be recognized at a point in time. The specific point in time can be determined by any of the following indicators:

- Seller has a right to payment.

- Physical possession has been transferred to the buyer.

- Buyer has legal title to asset.

- Buyer has risks and rewards of owning the asset.

- Buyer has accepted the asset.

Takeaway #5: For some organizations, ASC 606 may change the timing of when revenue is recognized compared to GAAP existing today. Organizations need to understand the differences between point-in-time revenue recognition versus over-time revenue recognition. A checklist can be utilized to determine and document when contracts are to be recognized at a point in time versus over time.

6. Disclosure requirements

Gone are the days of the vague one-paragraph standard revenue recognition disclosure. While many organizations used similar boilerplate revenue recognition disclosure, the users of those financial statements were found wanting more information. To address this, ASC 606 beefs up the disclosure requirements, focused on three key areas:

Contracts With Customers

The focus is on:

- Segregating revenue from contracts with customers from other sources of revenues. For example, an organization that both sells and leases equipment should report those revenue streams separately.

- Describing the relationship between revenue recognized and changes in the entity’s total contract assets and liabilities during the reporting period.

- Describing the entity’s performance obligations.

Significant Judgments

The disclosure requirements aim to answer the following questions:

- How and when are performance obligations satisfied?

- How is the transaction price determined and allocated to the performance obligations? What inputs are involved in the process?

Assets Recorded for the Costs to Obtain or Fulfill a Contract

This is an optional disclosure for nonpublic entities, but the underlying costs recorded in relation to obtaining a contract should be deferred and amortized, and the accounting policy should be disclosed in the notes to the financial statements.

Takeaway #6: Get in front of the coming tide. Do not expect your auditor to provide a sufficient boilerplate template for disclosures. ASC 606 is a principles-based standard applying to all industries. Organizations will need to use their judgment when applying the guidance of ASC 606 to the specific facts and circumstances of their contracts to recognize revenue. ASC 606 requires organizations to disclose the significant judgements that impacted the amount of revenue recognized during the reporting period.

Conclusion

The standard is effective for periods beginning after December 15, 2017, for public entities, which include not-for-profit entities that have issued or are a conduit bond obligor for securities that are traded, listed, or quoted on an exchange or an over-the-counter market. The standard is effective for all other entities effective for periods beginning after December 15, 2018.

If your organization has not started evaluating the impact of ASC Topic 606, we encourage you to begin now. This standard is quite long and will certainly impact your organization. For some industries, the revenue recognition standard may not ultimately change the amount of revenue that is recognized or the timing of recognition. However, the principles and process used to record that revenue absolutely will change under ASC 606.

When it comes to effectively implementing ASC 606, the devil is truly in the details. Each phase of the process requires significant judgment. Organizations will need to call on resources beyond their current accounting staff to ensure that internal systems, policies, and procedures address the myriad implementation challenges this standard presents.