Top two student loan planning options for healthcare professionals

Wipfli reports

As a healthcare professional, you have a very demanding career that doesn’t leave much time to look into your student loan repayment options.

On top of that, there aren’t many resources to turn to. Even if you reach out to your student loan servicer to ask questions, the person on the other end usually doesn’t have a wide depth of knowledge and experience to walk you through options specific to your situation.

That’s why we’re going to dive into two of the top student loan forgiveness programs for healthcare professionals: Public Service Loan Forgiveness (PSLF) and income-driven repayment (IDR) forgiveness.

Public Service Loan Forgiveness

PSLF is a 10-year program where after 10 years of making payments, your remaining student loan balance is forgiven, tax-free.

The PSLF program rolled out in 2007, but there wasn’t a lot of information at first about how to qualify, which has led to a high forgiveness denial rate. If you’re looking into PSLF, you absolutely must meet these three requirements:

- Have the right job: You must be a full-time employee at a U.S. federal, state, local or tribal government or 501(c)3 nonprofit organization.

- Have the right loans: You must have federal direct loans. If you have other types of federal loans, you should consolidate them into a federal direct loan before you start making the 120 total payments required under PSLF. Note that private loans do not qualify for PSLF.

- Have the right repayment plan: You must be on an income-driven repayment plan. Your options may include PAYE (pay as you earn), REPAYE (revised pay as you earn), IBR (income-based repayment) or ICR (income-contingent repayment).

PSLF requires you to make 120 qualifying payments total. They don’t have to be consecutive. You could leave your government or nonprofit organization and work for a for-profit organization for a few years — where your payments will not count towards PSLF — before going back to working for a government or nonprofit organization, where your payments would start to count again. You simply must meet all three requirements for an overall total of 10 years (aka 120 payments) to qualify for forgiveness of your remaining student loan balance.

In addition to making those 120 qualifying payments, you have to do two things on an annual basis:

- Submit the employment certification form: This verifies that each year you’re meeting the three qualifying requirements we covered above. If you submit the form but aren’t actually meeting one or more of the three requirements, you’ll have the form sent back to you. Then you’ll know you need to make a change to qualify.

- Recertify your income: Because you have to be on an income-driven repayment plan to qualify for PSLF, you need to use your most recent tax return to recertify your income online annually so that your monthly payments can be calculated based on your income.

Because PSLF is always based on your most recent tax return, which reflects last year’s income, it’s especially beneficial for someone entering their first year of residency to begin PSLF, since year one of the 120 payments is based on your previous year’s income as a student, which could be $0.

Let’s look at an example.

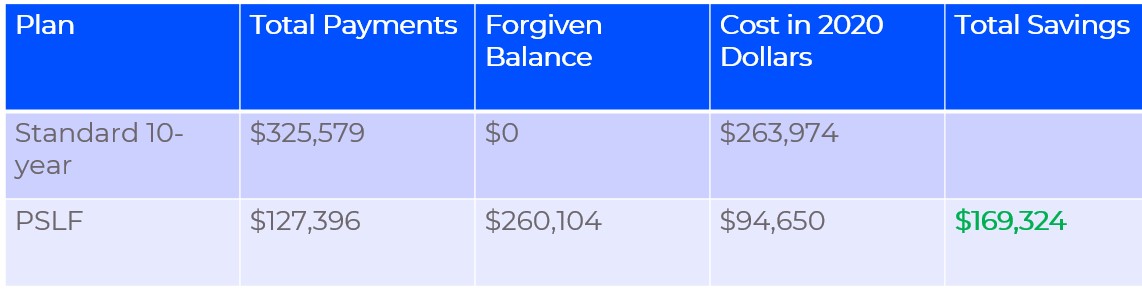

Say you’re a family practice physician resident with $250,000 in student loan debt. You’re a single borrower with no dependents, you have one direct, unsubsidized loan with an interest rate of 5.5%, and you’re on the REPAYE plan.

Here’s what your annual adjusted gross income (AGI) could look like over a 10-year period:

- $0 (based off last year’s tax return while you’re in school not making an income)

- $60,000 (the start of your three-year residency)

- $60,000

- $60,000

- $190,000 (here, your post-residency income increases)

- $200,000

- $210,000

- $220,000

- $230,000

- $240,000

With a default 10-year repayment plan, your monthly payment would be $2,713 a month (because you can’t possibly make this payment as a first-year resident, many people choose to go on forbearance, which only snowballs the total loan amount as interest starts adding up.)

But with the PSLF program, you pay $0 per month for the first year and $339 per month for the second year. It leads to huge savings over the 10 total years:

Note that while PSLF is more beneficial the lower your income is, generally, no matter where you are in your career, PSLF can be beneficial if you have $50,000 or more in federal student loans.

To see the savings example we put together of a physician assistant with $150,000 in student loan debt — aka someone later on in their career — watch our webinar, Healthcare Connections – Student loan forgiveness programs for medical professionals.

Income-driven repayment forgiveness

IDR is similar to PSLF, but it has some key differences. For one, you don’t have to work at a government or nonprofit organization. The two requirements you do have to meet are:

- Have federal direct loans.

- Be on an income-driven repayment plan.

IDR doesn’t have a 10-year repayment period like PSLF. Depending on which repayment plan you select, you’ll need to make qualifying monthly payments for either 20 years (240 payments total) or 25 years (330 payments total).

But like PSLF, you will need to annually recertify your income, since the income-driven repayment amount is based on your most recent tax return.

So, let’s look at an example in action.

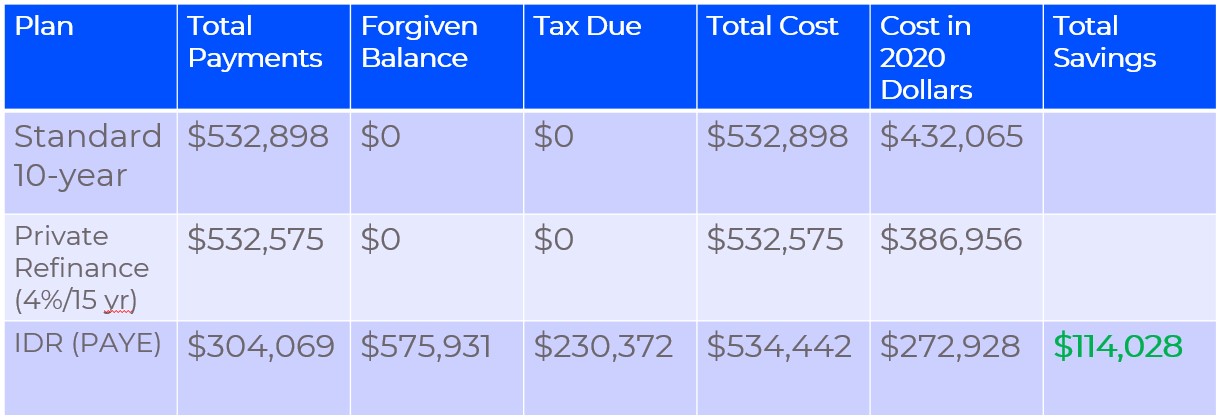

Say you’re a dentist with $400,000 in student loan debt. You’re married with no dependents, you have one direct, unsubsidized loan with an interest rate of 6%, and you’re on the PAYE plan (which has a 20-year repayment period).

If you use the split-income, married-filing-separately, community-property strategy (i.e., some community-property states allow you to move half of your income over to your spouse, which can lower your income total for the repayment calculation), your annual AGI could be:

- $125,00011 11. $185,030

- $130,00013 12. $200,129

- $135,20012 13. $192,431

- $140,60814 14. $208,134

- $146,23215 15. $216,459

- $152,08216 16. $225,117

- $158,16517 17. $234,122

- $164,49118 18. $243,487

- $171,07119 19. $253,227

- $177,91420 20. $263,356

If you are on the standard 10-year repayment plan, your monthly payment is a whopping $4,441. If you privately refinance, you could get that payment down to $2,959 per month.

But with IDR, your payment goes down to $830 per month for the first year. We recommend saving $617 a month into a taxable investment account to go towards the tax due on your forgiven balance. The $830 payment plus the $617 put away for future tax due equals $1,447 a month.

In this example, IDR leads to significant savings:

Unlike PSLF, IDR’s forgiven loan balance is taxable. The tax due on your forgiven balance of $575,931 could come to $230,372 if you are in the highest current income tax brackets. There are also likely to be additional annual tax-preparer costs and potentially more income tax due from filing your tax return married-filing-separate that should be considered. Even with these additional costs factored in, there are still substantial savings available with this strategy.

Generally, the people who benefit most from IDR are those who work for for-profit healthcare organizations and have a loan balance of $50,000 or greater.

Tax-planning strategies

The PSLF and IDR examples we gave above don’t include tax-planning strategies. The good news is, tax-planning strategies can increase your total savings. For example, if you make HSA contributions or pretax retirement account contributions, those lower your annual adjusted gross income and thus lower your monthly student loan payments and increase your total amount of loan forgiveness.

Answering more student loan forgiveness questions

There’s a lot to cover on this topic. We go even more in depth in our webinar, Healthcare Connections – Student loan forgiveness programs for medical professionals. There, you can find even more information on PSLF, IDR and other forgiveness options, as well as get answers to questions like:

- Can I combine PSLF or IDR with other loan assistance programs such as National Health Service Corps (NHSC) or Nurse Corps Loan Repayment?

- What impact has the CARES Act had on student loans, how do you know if your loans qualify and what actions should you take right now?

How we can help

The team at Wipfli specialized in challenges facing healthcare professionals and organizations today. Learn more on our healthcare services web page.