Accounting for PPP loans: Is it a loan or a grant?

When accounting for Paycheck Protection Program (PPP) loans, the first step for management is determining what type of transaction this is. Is it a loan, or is it a grant? Making this decision is the responsibility of management and will directly impact the accounting for the transaction.

Let’s explore each option.

Option 1: Loan

If management determines that it is a loan, the accounting answer is relatively simple: You would follow the guidance in ASC 470 and record the loan as a liability until the borrower is legally released from their obligation to repay the loan (i.e. the borrower has received notification of forgiveness from the SBA). At that time, the loan is removed from the books and income is recognized. However, as you get towards the end of the reporting period and even after the reporting period, more questions arise.

If the loan is forgiven after year end, but before the financial statement issuance date, how is the transaction presented?

The standards (ASC 405-20-40-1) are clear that you do not derecognize the loan until you’re legally released from the liability, making this a Type II subsequent event that would only be disclosed in the footnotes to the financial statements and not recorded in the income statement. Thus, if your business had a December 31, 2020 year-end and received forgiveness notification on January 5, 2021, the income related to the forgiveness would be recorded in 2021. There would be a footnote only at 12/31/2020, and the loan would remain on the balance sheet at 12/31/2020.

How should you present the short-term and long-term portions of this note?

Typically, the short-term and long-term portions of debt are based on the loan agreement that governs the payments. Since PPP loans have a loan agreement, the first step would be to read that agreement. The next step would be to understand that certain laws that have been enacted can trump GAAP. The Paycheck Protection Program Flexibility Act, signed into law in 2020, does note that a company has a 10-month period after the elected covered period expires to file for forgiveness, and during this period, no payments are required to be made.

Additionally, the master glossary definition of a current liability in ASC 210-10-45 does state that current liabilities are obligations whose liquidation is reasonably expected to be completed within one year.

Based on these items, you may conclude that the PPP loan liability does not meet the definition of a current liability, and thus would be treated as a noncurrent liability.

Do you need to impute interest at a market rate, since the loan has a stated rate of 1%, which is below market?

No, there is an exemption for this in ASC 835-30-15-3(3). The interest expense at 1% should be accrued, but you would not need to compute and record any imputed interest.

How should this be recorded on the statement of cash flows?

The cash inflow should be recognized in the financing section of the statement of cash flows. If the loan forgiveness notification was received prior to the end of the reporting period and the income has been recognized in the income statement, there would be a noncash adjustment in the operating section to reflect this, similar to how we would present a gain transaction.

Option 2: Grant

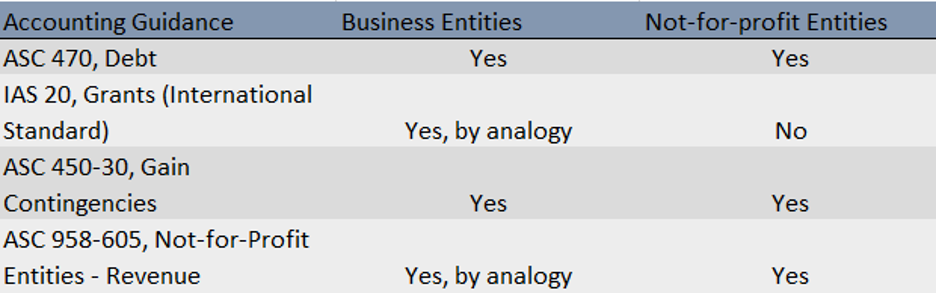

If management determines that the PPP loan is not really a loan in substance, but rather a governmental grant, the accounting options available would depend on the type of reporting entity. See the chart below for accounting options available. Note that a nonprofit entity is not allowed to analogize to IAS 20 because they have existing GAAP for this type of transaction, documented in ASC 958-605.

For-profit entities do not have existing GAAP for governmental grants, so they are allowed to analogize to other GAAP, either by applying ASC 958-605, or by looking to international standards, specifically IAS 20.

Considerations for nonprofits: As noted above, nonprofits can consider the PPP loan a loan and then fall under the guidance in ASC 470. But if they feel that a grant is the more accurate accounting model for this transaction, they would apply ASC 958-605. Under this model, conditional grants are not recognized into income until the conditions are substantially met or explicitly waived.

The one tricky area here is determining what the conditions of the grant are and what actions are deemed to be “trivial” tasks in the grant process. There are currently three schools of thought:

- There is only one condition: Incurring the eligible expenses to qualify for forgiveness.

- There are two conditions: Incurring the eligible expenses to qualify for forgiveness AND the application for forgiveness has been completed and remitted.

- There are three conditions: Incurring the eligible expenses to qualify for forgiveness AND the application for forgiveness has been completed and remitted AND the SBA has approved the application for forgiveness along with the supporting documentation.

Determining which of these scenarios is applicable is a judgement call by management. Once management determines that the conditions of the grant have been met, the borrower can recognize the income associated with the PPP, usually as “grant revenue” for a nonprofit entity. Prior to recognition of the income, the PPP is recognized as a “refundable advance” on the balance sheet.

Considerations for for-profit entities: For-profit entities can choose to either analogize to ASC 958-605 (described above) or potentially analogize to IAS 20. For entities analogizing to IAS 20, they would recognize revenue as the expenses are incurred if it is probable that the conditions attached to the assistance will be met and assistance will be received. A liability would remain for any portion of the funds that have not been expended at the balance sheet date.

Cash Flows: Grant

If management has determined that the transaction is best represented as a grant, the transaction would be recorded entirely within the operating section of the statement of cash flows. If income has been fully recognized, there will be no special line item on the statement of cash flows, because the income is already recorded and thus no reconciliation is necessary in the statement of cash flows.

Closing thoughts

We did not cover one potential option, and that is ASC 450-30, Gain Contingencies. We do not foresee many companies applying this GAAP, but if they do, the accounting would be very similar to that of ASC 470, where a liability would remain until the forgiveness notification was received.

When it comes to recognizing the income — whether recording as grant under IAS 20 or ASC 958-605 or an extinguishment of debt under ASC 405-20 — the income should be presented separately in the income statement if the amount is material. Netting the forgiveness with the incurred expenses is not permitted by GAAP.

Additionally, whatever method is chosen by management, disclosure in the footnotes is imperative. Even if the transaction was completed (forgiveness received) prior to the end of the reporting period, the accounting method chosen (loan vs. grant) would impact how the transaction is presented in the statement of cash flows. At a minimum, in addition to disclosing the accounting policy, the disclosures should include the amount received, the amount included in income and remaining in liability (if any), and the remaining conditions to be met (if applicable).

If you have any questions about accounting for PPP loans, contact us for assistance.

Related content:

How financial institutions should handle accounting for PPP loan fees

IRS issues guidance on when a taxpayer can deduct PPP-funded expenses

PPP and other SBA loan provisions in Consolidated Appropriations Act of 2021

The Consolidated Appropriations Act of 2021: Great news for 501(c)(6) nonprofits