What does a flat yield curve mean for your financial institution?

The U.S. Treasury finances federal government budget obligations by issuing debt. The Treasury market includes notes of varying maturities ranging from one month to 30 years. Typically, the yields on Treasuries slope upward as investors require better returns for taking risks on longer-term cash flows. Most often, the 10-year rate is higher than the two-year rate. The “2-10” is a common rate comparison to indicate the steepness of the Treasury yield curve.

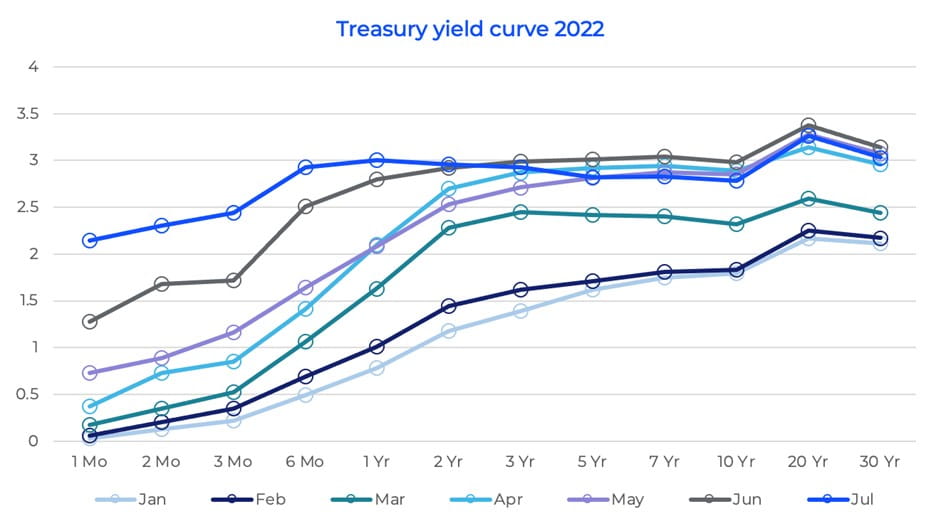

Market interest rates are often talked about as if all maturities move together, but that is not the case. Rates of different maturities move independently, which means that the yield curve will periodically flatten or invert. A flat yield curve is just that — yields for short-term maturities are similar to yields for longer-term maturities. This has been the case in 2022, as the two-year and 10-year yields first briefly inverted in April, then inverted again in July.

A flat or inverted yield curve can mean a variety of things, but it has typically been not-so-good news for the economic outlook and has foreshadowed previous recessions. Below, you can see how the yield curve slope has changed over the course of the year as the Federal Reserve has moved its benchmark interest rate to combat inflation:

Source: Resource Center | U.S. Department of the Treasury

The Federal Reserve’s benchmark interest rate affects short-term rates directly, which is why short-term rates moved up. However, the 10-year Treasury operates with different mechanics. The 10-year is impacted by long-term growth outlook, global economics and other market forces.

ALCO agenda

Your financial institution’s asset/liability committee (ALCO) should be aware of moves in the Treasury yield curve. The Treasury yield curve is known as the “risk-free rate” and influences pricing across the market. But why should the ALCO be aware of this?

Of course, there are everyday implications. For example, the ALCO may be discussing whether the U.S. is heading into a recession, and if so, how the institution should prepare itself and customers/members. It may also be discussing the rate impact on overnight deposits/shares, the impact of economic changes on loan and deposit/share demand, or what is happening to the unrealized gain or loss on the investment portfolio.

Among the interest-rate risk implications that the ALCO should be aware of most importantly are changes to net interest margin. The ALCO should understand which products price off of the short end of the yield curve. Overnight correspondent balances, negotiable order of withdrawal (NOW) accounts and variable-rate home equity loans will usually move closer in line with the two-year Treasury, while products that price off the long-end of the curve like mortgage rates or long-term borrowings will move more in line with the 10-year. When the yield curve inverts, pricing on products will not move in lockstep.

Potential impacts to interest-rate risk model results

For your interest-rate risk models, many financial institutions are seeing significant increases to their economic value of capital results. Low-cost deposits and shares that are valued based on overnight or short-term rates will see positive gains in economic value. At the same time, the assets priced off the longer end of the curve may experience smaller losses in value.

These economic value changes will ultimately be impacted by how much and how quickly you move rates on your products, in conjunction with continued market rate changes. Before adopting strategies regarding interest-rate risk, the ALCO should understand how the market rate changes impact the value of its products.

Net-interest income projections have changed as well. Offering rates applied to new volumes in the model are often driven off of market pricing for products with similar duration. As short-term rates moved up, most financial institutions saw higher projected costs on deposits or shares being offset by increased yields on overnight correspondent balances and variable-rate home equity loans, for example. Your ability to capitalize on these rate changes will come down to your strategy, pricing power and timing.

Managing changing rates

The timing and magnitude of your financial institution’s price changes must be actively managed to maintain the net interest margin. The ALCO should discuss and set strategy on how to price your loans and deposits or shares when rates are changing quickly. Is your pricing principle-based, formula-based, or does it change arbitrarily?

Set a minimum frequency of at least quarterly to review pricing. The ALCO should be proactive and thoughtful to avoid chasing the market.

The ALCO should regularly review the pricing assumptions in your interest-rate risk model. Your repricing assumptions (betas) for loans and deposits or shares may be different today than they were last year. Understanding those behavioral differences can influence risk-taking decisions. There could be pent-up rate demand: Will your customers/members demand higher deposit/share rates since they’ve seen so much talk about higher rates? What is the price elasticity for your loan rates? At what rate will demand for loan dollars start to slow?

The ALCO should review the impact of a variety of non-parallel yield curve changes as well. Your base-case model is shocking up and down from a point-in-time yield curve, which as of now is pretty flat. The ALCO should also understand what happens to your balance sheet position if long-term interest rates increase at a faster rate than short-term rates (bear steepener), or if short-term interest rates fall faster than long-term rates (bull steepener).

In addition, the ALCO should be reviewing the composition and maturity ladders of its assets and liabilities. The ALCO should discuss its funding strategy and asset composition and how it may be impacted by changing rates. When the interest rate outlook is uncertain, one of the best strategies is to ladder maturities to achieve more evenly distributed cash flows. This allows reinvestment in various interest rate environments.

In the months ahead, the upward sloping yield curve could return, or it could be inverted further. Either way, the same principles hold true.

Tips for managing uncertainty

These points can help the ALCO successfully navigate quickly changing interest rates:

- Understand the everyday implications of changing rates. What does it mean for your customers/members, the broader economy and the institution?

- Understand how rate changes are impacting the interest rate risk model results.

- Have a proactive loan and deposit/share pricing strategy that is updated more frequently than quarterly to maintain the institution’s net interest margin position.

- Review and update impacted assumptions in the interest rate risk model that can influence future risk-taking decisions.

- Assess your exposure to future rate changes by understanding the impact of various market interest rate environments (parallel shocks and non-parallel shocks).

- Review asset and liability composition and ladder maturities when the rate outlook is uncertain.

While it’s not the ALCO’s job to predict what will happen from here, the committee can help prepare the financial institution to thrive under various scenarios. These tips, in addition to your normal ALCO activities (modeling, reviewing assumptions, sensitivity and stress testing, and backtesting), will help the ALCO set some groundwork to navigate a shifting rate environment.

How Wipfli can help

A shifting economy along with unpredictable changes in Treasury yields make this an opportune time to assess the implications of changing interest rates and how your pricing strategy for loan products, deposits or shares may be affected. Wipfli professionals can help you review your approach to ensure you are best meeting the needs of your customers/members and the needs of your institutions

Contact us to learn more about the guidance we provide to financial institutions. Sign up to receive more insights relevant for financial institutions or continue reading on: