“These projections are realistic, but there are a lot of variables,” said Anna Kooi, partner and financial services practice leader at Wipfli. “If firms are counting on market performance or M&A to support growth, that’s outside their control. The levers they can control — like driving organic growth — have been harder to activate.”

Meanwhile, complexity has intensified. Firms are facing intersecting pressures — from evolving compliance expectations to shifting market dynamics and accelerating technology demands.

“Firms are optimistic, but they’re also managing more moving parts than ever before,” Kooi said. “Success depends on how well leaders can prioritize and execute amid all that noise.”

Technology could help close that gap.

“Tools that enhance how advisors personalize client interactions, anticipate client needs and deepen relationships can be just as valuable as tools that improve back-office efficiency,” Kooi said. “Firms can’t get away from making investments in technology, data analytics and AI.”

Nearly nine in 10 (89%) wealth management respondents said they use AI and data analytics to support decision-making. Almost half (49%) reported using real-time insights to guide automated decision-making and business strategy, and 40% said they use predictive models and dashboards.

Respondents also identified barriers to implementing data analytics effectively. Data privacy and security were cited most often, followed by data quality issues and integration with existing systems.

Most respondents reported using AI in some capacity, but few have advanced to true enterprise readiness. “A lot of firms are experimenting,” Kooi said. “They may have AI embedded in certain tools or workflows, but that’s not the same as having a roadmap that ties back to business strategy.”

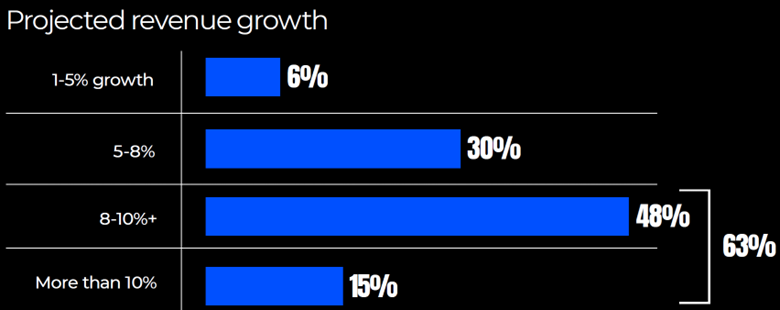

Nearly all respondents expect their firm’s revenue to grow in the next 12 months. About two-thirds projected growth of 8% or higher.

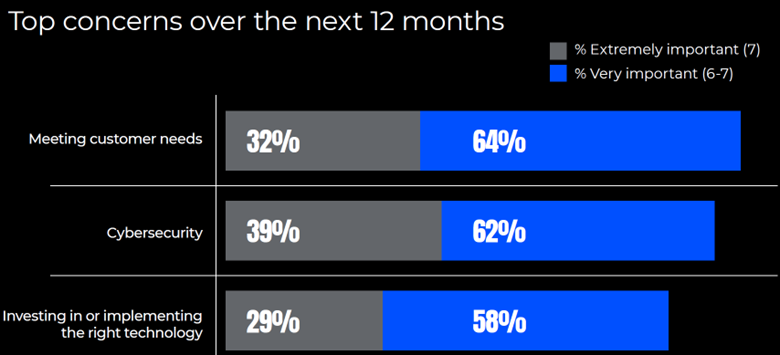

When respondents rated their level of concern across a range of issues, technology-related factors consistently ranked near the top.

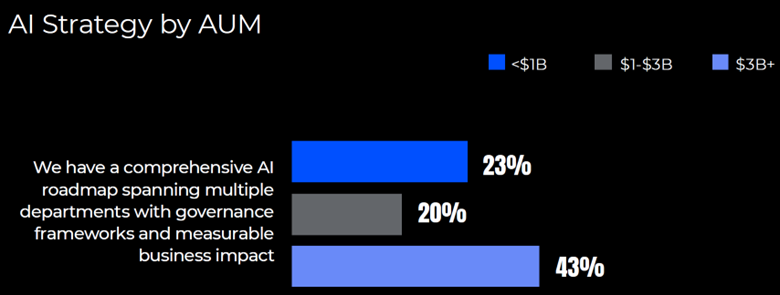

Most respondents said their firms are actively implementing AI solutions in targeted areas with defined goals and metrics. Respondents from large firms were significantly more likely to report having a comprehensive AI roadmap.

Covered in the full report

- Growth expectations: Nearly all respondents expect revenue growth in the next 12 months, and 63% expect gains of 8% or more.

- Growth drivers: Data analytics, digital customer engagement and automation were the top-ranked growth strategies — cited by respondents from every firm size.

- Cybersecurity: For the third year in a row, cybersecurity ranked as a top concern.

- Technology: Nearly two-thirds of respondents said cybersecurity, data privacy measures and account management platforms have a “large” or “major impact” on how they do business.

- AI strategies: Most respondents report implementing AI solutions or having a comprehensive AI roadmap — but far fewer have achieved enterprise-wide government or the measurement needed for true maturity.

- Next steps: Wipfli advisors add context and offer strategies to help wealth management leaders maintain their confidence and achieve their goals amid a complex and changing environment.

Download the full report for deeper analysis and an appendix with all the data. For media inquiries, contact Alicia O’Connell at alicia.oconnell@wipfli.com.

Download the full report