Summarizing all 11 of the FASB’s 2020 Accounting Standard Updates

The year 2020 has introduced the world to a number of new terms and phrases — including “pandemic,” “social distancing,” “lockdown” and “quarantine.” The economic circumstances behind these terms generated an onslaught of accounting challenges for standard setters, users and preparers of financial statements.

Despite the challenges imposed by COVID-19, the Federal Accounting Standards Board (FASB) remained vigilant and issued 11 Accounting Standard Updates (ASUs) throughout 2020. Some of the ASUs are a direct result of the pandemic, while others are based on ongoing projects undertaken by the FASB and staff.

Below is a high-level summary of the ASUs issued in 2020, including the rationale for the standard, the applicability and the effective dates.

ASU 2020-01 – Investments – Equity Securities (Topic 321), Investments – Equity Method and Joint Ventures (Topic 323), and Derivatives and Hedging (Topic 815)

ASU 2020-01 provides additional guidance in response to questions raised by stakeholders as a result of the adoption of ASU 2016-01, which added Topic 321, Investments – Equity Securities and provided an entity with the option to measure certain equity securities without a readily determinable fair value at cost, minus impairment.

The introduction of this measurement alternative created confusion among stakeholders about when the equity method of accounting in Topic 323 would apply versus the use of the measurement alternative afforded by ASU 2016-01.

Another concern raised by stakeholders related to the interaction between Topics 321, 323 and 815 when applying the guidance to certain forward contracts and purchase options that would be accounted for under the equity method of accounting.

ASU 2020-01 amended the current guidance to specifically address the issues raised by stakeholders for when to apply Topic 321, Topic 323 and Topic 815. In particular, the FASB clarified that entities seeking to apply the measurement alternative found in Topic 321 should first consider whether there are observable transactions that would require the reporting entity to either apply or discontinue the equity method of accounting in accordance with Topic 323. With respect to certain forward contracts and purchase options, the FASB explained an entity should not consider whether the underlying securities would be accounted for under Topic 323 or the fair value option found in Topic 825 upon the settlement of the contract or purchase option. Entities should instead consider the characteristics of these contracts and options based on the guidance found in 815-10-15-141 to determine the appropriate accounting treatment.

The amendments found in ASU 2020-01 apply to all entities that apply the guidance found in Topics 321, 323 and 815; elect to apply the measurement alternative in Topic 321; or enter into certain forward contracts or purchase options that would be accounted for under the equity method of accounting. The amendments are to be applied prospectively and are effective for public business entity fiscal years beginning after December 15, 2020, and fiscal years beginning after December 15, 2021, for all other reporting entities. Early adoption is permitted for public business entities for periods in which financial statements have not been issued and for other entities in periods in which financial statements are not yet available for issuance.

ASU 2020-02 – Financial Instruments – Credit Losses (Topic 326) and Leases (Topic 842)

ASU 2020-02 amended the accounting guidance in response to SEC Staff Accounting Bulletin Number 119 and provides useful information for the application and reporting requirements of the Current Expected Credit Losses (CECL) standard Topic 326.

Specifically, the amendments provide:

- A description of the measurement process for current expected credit losses.

- Interpretive responses to questions surrounding the development, governance and documentation of a systemic methodology when applying CECL.

- Guidance on the appropriate documentation of the results and validation of the systematic methodology applied.

With respect to ASU 2016-02, Leases (Topic 84), ASU 2020-02 clarified that a public business entity that would otherwise not meet the definition of a public business entity, except for a requirement to furnish financial information to the SEC in another entity’s filing, to adopt Topic 842 for fiscal years beginning after December 15, 2020, and interim periods within fiscal years beginning after December 15, 2021. These effective dates are consistent with the effective dates of the standard found in ASU 2019-10, Financial Instruments – Credit Losses (Topic 326), Derivatives and Hedging (Topic 815), and Leases (Topic 842): Effective Dates.

The guidance in this ASU applies to all entities with transactions that fall within the scope of Topic 326 or Topic 842 and did not modify the effective dates for these accounting standards.

ASU 2020-03 – Codification Improvements to Financial Instruments

As an ongoing project, the FASB continually seeks to improve and further clarify the guidance found in the FASB Accounting Standards Codification. ASU 2020-03 provides a number of amendments to the Codification across a variety of topics. These topics include:

- Fair value option disclosures

- Applicability of the Portfolio Exception in Topic 820 to nonfinancial items

- Disclosures for depository and lending institutions

- Cross-reference to line-of-credit or revolving-debt arrangements guidance found in Subtopic 470-50

- Cross-reference to net asset value practical expedient in Subtopic 820-10

- Interaction of Topic 842 (Leases) and Topic 326 (CECL)

- Interaction of Topic 326 (CECL) and Subtopic 860-20 (Transfers and Servicing – Sale of Financial Assets)

The amendments found in ASU 2020-03 are applicable for entities with transactions in the scopes of the various Topics and Subtopics. Topics 1 through 5 represent conforming amendments that are effective upon issuance of the ASU for public business entities and all other reporting entities for fiscal years beginning after December 15, 2019.

Topics 6 and 7 affect the guidance found in ASU 2016-13, CECL (Topic 326). For entities that have not yet adopted the guidance in ASU 2016-13, the effective dates are consistent with the dates found in ASU 2016-13. For entities that have adopted ASU 2016-13, the amendments are effective for fiscal years beginning after December 15, 2019 and should be applied on a modified-retrospective basis through a cumulative-effect adjustment to opening retained earnings as of the date the entity adopts ASU 2016-13.

ASU 2020-04 – Reference Rate Reform (Topic 848)

In response to concerns raised about the effects of reference rate reform, the FASB issued ASU 2020-04 to provide additional guidance and relief for stakeholders upon adoption.

Reference rate reform resulted from the announcement by the United Kingdom’s Financial Conduct Authority that banks will no longer be required to utilize LIBOR as of the end of 2021. Currently, many contracts — including loans, lease agreements, hedges and other financial instruments — incorporate the use of LIBOR and must now transition to a new reference rate.

For U.S. GAAP, the Secured Overnight Financing Rate (SOFR) has been identified as the preferred alternative to LIBOR. Stakeholders raised concerns about the transition to the new rate and whether the change results in the termination or modification of existing contracts. This would require significant time and effort to assess contracts under current GAAP and ensure the appropriate accounting treatment is applied upon transition. In addition, stakeholders raised concerns specific to hedge accounting and wondered whether changes in the reference rate could disallow the application of certain hedge accounting guidance, resulting in specific hedge relationships no longer qualifying as highly effective.

The amendments within ASU 2020-04 provide optional expedients and exceptions in the application of reference rate reform to existing contracts. These expedients including the following:

- Prospective application for debt and receivable contracts within the scope of Topic 310 and 470, respectively, without extinguishment or modification of the existing agreement

- Option to not treat the change in reference rate as a new or modified lease for leases within the scope of ASC 840 and 842

- Ability to elect not to reassess original conclusions reached regarding embedded derivatives that are clearly and closely related to the host for contracts within the scope of Subtopic 815-15, Derivatives and Hedging – Embedded Derivatives

Topic 848 also includes general guidance that allows an entity to forego contract remeasurement or reassessment solely due to the change in the reference rate as well as specific expedients for excluded components, fair value hedges, cash flow hedges and debt classified as held to maturity. Upon election, the optional expedients must be applied consistently for all eligible contracts.

The amendments in this ASU are applicable to all entities with contracts that fall within the scope of Topic 848 or have contracts with references to a reference rate expected to be discontinued. ASU 2020-04 is effective for all entities as of March 12, 2020, through December 31, 2022, at which time transition is expected to be complete. Entities are allowed to apply the amendments as of any date from the beginning of an interim period including or subsequent to March 12, 2020, up to the date that the financial statements are available to be issued. Once elected, the amendments must be applied prospectively for all eligible contract modifications under that specific Topic or Industry Subtopic.

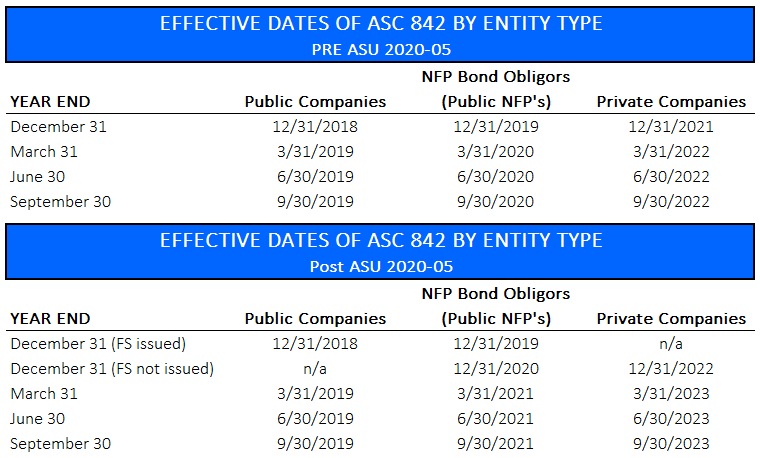

ASU 2020-05 – Revenue from Contracts with Customers (Topic 606) and Leases (Topic 842)

Due to the economic and financial burden imposed on entities across the globe resulting from the COVID-19 pandemic, the FASB issued ASU 2020-05, which defers the elective date for Revenue Recognition (Topic 606) and Leases (Topic 842) for specific entities.

Though all public business entities, certain nonprofit entities and certain employee benefit plans were required to adopt Topic 606 for years beginning after December 15, 2017, private business entities were not required to adopt this standard until their fiscal years beginning after December 15, 2018. Therefore, many private entities were required to adopt in calendar year 2020 among the turmoil induced by COVID-19. In an effort to provide relief, the FASB deferred the adoption date of Topic 606 for one more year for all private companies that had not yet issued their 2019 financial statements as of June 3, 2020.

ASU 2020-05 also deferred the effective date for Topic 842, Leases, for all those entities that were not already required to adopt the new standard or elected early adoption. ASU 2019-10 had previously deferred the original effective date for the new lease standard for other reporting entities for fiscal years beginning after December 15, 2020. The additional deferral introduced by ASU 2020-05 is summarized in the table below.

The amendments to the effective dates in ASU 2020-05 are effective as of June 3, 2020 and are applicable to all entities. Private companies that have already adopted Topic 606 or Topic 842 and issued financials for fiscal year 2019 are not eligible to apply the additional deferral election.

ASU 2020-06 – Debt – Debt with Conversion and Other Options (Subtopic 470-20) and Derivatives and Hedging – Contracts in Entity’s Own Equity (Subtopic 815-40)

Accounting for financial instruments with characteristics of liabilities and equity is a complex area of GAAP in which financial statement preparers continually struggle when applying the current accounting guidance.

For convertible instruments (convertible debt and convertible preferred stock), there is often confusion and inconsistent conclusions reached when applying the accounting models in the current guidance. As a result, the FASB reduced the number of accounting models under this analysis.

Prior to the release of ASU 2020-06, an embedded derivative or substantial premium that qualified for a scope exception to not be separately presented from the host instrument, would then have to be assessed for separate treatment due to the existence of a cash conversion or beneficial conversion features. ASU simplified the guidance in ASC 815-15 by no longer requiring the assessment of these features for separation from the host based on the existence of a cash conversion or beneficial conversion feature (BCF) if one of the scope exceptions is met.

The Board also improved the consistency of the EPS guidance by requiring the if-converted method to be used for convertible instruments when computing diluted EPS, as well as:

- Requiring the inclusion of the effect of potential share settlement.

- Including equity-classified convertible preferred stock with a down round feature.

- Clarifying that an average market price should be used to compute the diluted EPS denominator when exercise prices may change based on an entity’s share price or changes in the share price may affect the number of shares upon settlement.

- Requiring the use of the weighted-average share count from each quarter when calculating the year-to-date weighted-average share count.

The amendments in this ASU apply to all entities that issue convertible instruments and/or contracts in an entity’s own equity and any entity required to report diluted EPS for instruments that may be settled in cash or shares. ASU 2020-06 is effective for public business entities meeting the definition of a SEC filer, excluding smaller reporting entities, for fiscal years beginning after December 15, 2021. For all other entities, the effective date is for fiscal years beginning after December 15, 2023. Early application is permitted but no earlier than fiscal years beginning after December 15, 2020.

ASU 2020-07 – Not-for-Profit Entities (Topic 958)

In order to increase the transparency of contributed nonfinancial assets, the FASB issued ASU 2020-07, which enhances the presentation and disclosure requirements for NFP entities.

Contributed nonfinancial assets include donated fixed assets, materials, supplies, donated use of fixed assets, intangible assets, gifts-in-kind (contributed services) and any unconditional promises of those assets. The amendments in this ASU require NFPs to separately present contributed nonfinancial assets on the face of the statement of activities, as well as:

- Disclose a disaggregation of the amounts of contributed nonfinancial assets recognized in the statement of activities by category.

- Provide additional disclosures, including certain qualitative information about the use of contributed assets, the NFP’s policy with respect to these assets, a description of any donor-restrictions, and other information listed in ASU 2020-07.

The amendments in this accounting standard are applicable to all NFPs that receive or have received contributed nonfinancial assets. ASU 2020-07 is required to be applied on a retrospective basis and is effective for annual periods beginning after June 15, 2021, with early adoption permitted.

ASU 2020-08 – Codification Improvements to Subtopic 310-20, Receivables – Nonrefundable Fees and Other Costs

The amendments to the guidance in ASU 2020-08 provide a more detailed explanation on the subsequent measurement of callable debt and whether callable debt falls within the scope of paragraph 310-20-35-33. ASU 2020-08 applies to all entities with callable debt and is effective for public business entities for fiscal years beginning after December 15, 2020, with early adoption not permitted. For all other entities, the amendments are effective for fiscal years beginning after December 15, 2022, with early adoption permitted in fiscal years beginning after December 15, 2020.

ASU 2020-09 – Debt (Topic 470)

ASU 2020-09 amends and supersedes certain SEC content within the Accounting Standards Codification to align the guidance with the information contained in SEC Release No. 33-10762. The amendments mostly apply to Topic 470 and relate to financial disclosure requirements for SEC registrants and other entities required to furnish information with the SEC. The updates in this amendment are applicable for all SEC registrants and are effective as of January 4, 2021, with early application permitted.

ASU 2020-10 – Codification Improvements

The FASB issued ASU 2020-10 to further clarify and improve the Codification by codifying all guidance that requires or provides the option for an entity to disclose information within the footnotes. This clarification is meant to reduce the likelihood of a preparer missing required disclosure requirements.

In addition, ASU 2020-06 included other improvements to the codification across a variety of areas, including updates to the Master Glossary, interim reporting requirements, receivables guidance within Subtopic 310-10 and other areas of GAAP.

While the amendments do not introduce new topics or subtopics or change existing GAAP, all entities should review the changes found in the ASU to assess the impact it may have on their financial reporting requirements.

Amendments are effective for public business entities for fiscal years beginning after December 15, 2020, and all other entities beginning after December 15, 2021. Early application is permitted for all financial statements not yet issued for public business entities and financial statements not yet available for issuance for all other entities. The amendments should be applied on a retrospective basis as of the beginning of the period including the adoption date.

ASU 2020-11 – Financial Services – Insurance (Topic 944)

In order to alleviate the financial reporting burden in the midst of the global pandemic, the FASB issued ASU 2020-11, which defers the effective date of ASU 2018-12, Financial Services – Insurance (Topic 944): Targeted Improvements to the Accounting for Long-Duration Contracts (LDTI).

ASU 2020-11 defers the effective date for implementation of LDTI by one year for all insurance companies and provides transitional relief to facilitate early application and provide better information to investors and other financial statement users. For entities choosing early adoption, the application of LDTI may be applied as of the beginning of the prior period or as of the beginning of the earliest period presented.

The amendments apply to all insurance companies and are effective for fiscal years beginning after December 15, 2022 for public business entities that qualify as an SEC filer. For all other reporting entities, LDTI is effective for fiscal years beginning after December 15, 2024.

Questions about any of these Accounting Standard Updates?

If you have any questions about the 11 ASUs the FASB issued in 2020, contact Wipfli for help. Or continue reading on:

Accounting for COVID-19-related loan modifications