Understanding the new lease guidance

In February 2016, the Financial Accounting Standards Board (FASB) issued Accounting Standards Update (ASU) 2016-02 Leases (Topic 842). Topic 842 defines a lease as “a contract, or part of a contract, that conveys the right to control the use of identified property, plant, or equipment (an identified asset) for a period of time in exchange for consideration.” Users of financial statements have criticized the fact that previous GAAP did not provide the full representation of operating lease transactions, which led to the FASB issuing this new standard. The key principle of Topic 842 is that lessees should recognize the asset and liability that arises from a lease. The asset that is recognized is termed a right-of-use (ROU) asset, and the corresponding liability represents the future lease payments.

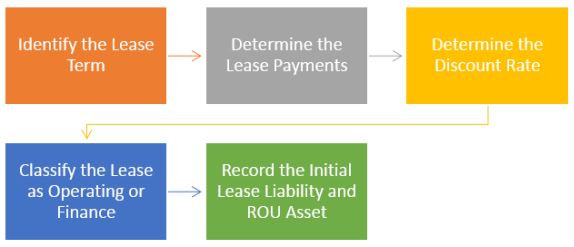

When determining the proper accounting for a lease under Topic 842, the following steps should be taken:

Lease Term

An entity should consider the noncancelable period of a lease. Optional periods to extend a lease should also be considered if at the commencement date lessees are reasonably certain to exercise their option to extend the lease.

Lease Payments

Lease payments include fixed payments (less any lease incentives), variable payments, and the exercise price of a purchase option if lessees are reasonably certain to exercise their option.

Discount Rate

From a lessee’s perspective, the discount rate is the rate implicit in the lease unless that rate cannot be readily determined. In that case, lessees are required to use their incremental borrowing rate.

Operating vs. Finance Leases

Under Topic 842, leases from a lessee’s perspective are classified as operating or finance leases. The criteria for distinguishing between these two types of leases are substantially similar to the criteria for distinguishing between operating and capital leases under previous GAAP. Lessees should classify a lease as a finance lease if it meets any of the following criteria at the commencement of the lease:

- Ownership transfers to the lessee will occur by the end of the lease term.

- The lessee has an option to purchase the underlying asset and is reasonably certain to exercise it.

- The lease term is for the major part of the remaining economic life of the underlying asset.

- The present value of the sum of the lease payments equals or exceeds the fair value of the underlying asset.

- The underlying asset is expected to have no alternative use to the lessor at the end of the lease.

Transition Guidance

ASU 2016-02 is effective for public business entities and not-for-profit entities that have issued or are a conduit bond obligor for securities that are traded, listed, or quoted on an exchange or an over-the-counter market for fiscal years beginning after December 15, 2018. For all other entities, ASU 2016-02 is effective for fiscal years beginning after December 15, 2021, and interim periods within fiscal years beginning after December 15, 2022. Early adoption is permitted for all entities.

In transitioning to the new standard, lessees and lessors are required to recognize and measure leases at the beginning of the earliest period presented using a modified retrospective approach, which allows for optional practical expedients. An entity that elects to apply the practical expedients will, in effect, continue to account for leases that commenced before the effective date in accordance with previous GAAP unless the lease is modified, except that lessees are required to recognize a right-of-use asset and a lease liability for all operating leases at each reporting date based on the present value of the remaining minimum rental payments that were tracked and disclosed under previous GAAP.

While the application of this standard will impact primarily the balance sheet, companies should spend time now assessing how it will impact loan covenants and other contractual agreements. When entering into new debt agreements, be sure that covenants based on debt to equity or debt service coverage ratios are written such that the ratios will be adjusted when the standard becomes effective.

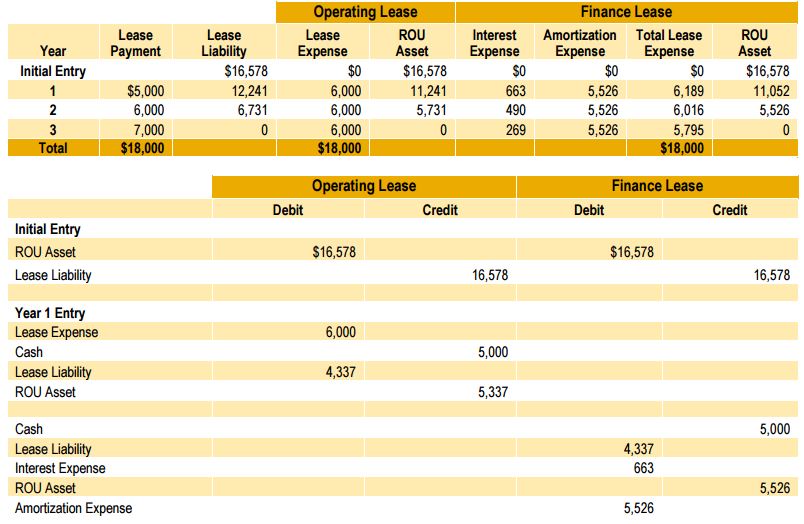

Below is an example to illustrate the accounting for an operating and finance lease:

- Lease Term: Three-year lease of a building, with the option of extending for an additional three years.

- Lease Payments: $5,000 in year one, $6,000 in year two, $7,000 in year three, and $8,000 each year during the optional periods.

- Discount Rate: The rate implicit in the lease is not readily determinable.

At the commencement of the lease, the lessee concludes that it is not reasonably certain to exercise its option to extend the lease and therefore determines the lease term to be three years. In addition, the lessee determines that its incremental borrowing rate is 4%, which is the rate at which the lessee could borrow a similar amount, for the same term, and with similar collateral as in the lease at the commencement date.

Notice that the lease liability is the same whether the lease is classified as operating or finance. The right-of-use asset balances are different, however. Under a finance lease, the right-of-use asset is amortized on a straight-line basis over the lease term. Under an operating lease, the right-of-use asset is amortized over the lease term by the difference between the straight-line lease expense and the interest expense.

The following table illustrates how the accounting for this lease would differ depending on the classification. Journal entries for the initial entry and year one for both types of leases have been included below.