SAS 134: Your audit report is changing — Are you ready?

For calendar year-end entities, your December 31, 2019, audit report may look a lot like what you are used to. But did you know that going forward, the look and feel of your audit report will be changing dramatically?

In May of 2019, the Auditing Standards Board (ASB) of the American Institute of Certified Public Accountants (AICPA) issued Statement on Auditing Standards (SAS) No. 134, Auditor Reporting and Amendments, including Amendments Addressing Disclosures in the Audit of Financial Statements.

What is SAS 134?

This new standard makes fundamental changes in the layout of the audit report, as well as the information required to be presented in all auditor reports issued under generally accepted auditing standards (GAAS). The standard is effective for reporting periods ending on or after December 15, 2020.

SAS 134 was issued by the ASB to: 1) converge GAAS with the auditor reporting standards promulgated by the International Auditing and Assurance Standards Board (IAASB) and 2) to create consistency with the revised auditor reporting model supported by the Public Company Accounting Oversight Board (PCAOB).

The revised reporting model is intended to enhance the communicative value and relevance of the auditor’s report to the users of the audited financial statements. It does this by: 1) providing more transparency into the audit and the related auditor’s report, 2) satisfying the user’s need for more information by addressing the auditor’s responsibility and 3) providing new guidance for the form and content of the auditor’s report.

Early adoption of this new auditor’s report is not allowed to prevent audit reports from being issued in different formats for the same reporting period.

What is SAS 134 changing?

So, what is changing in the auditor’s report?

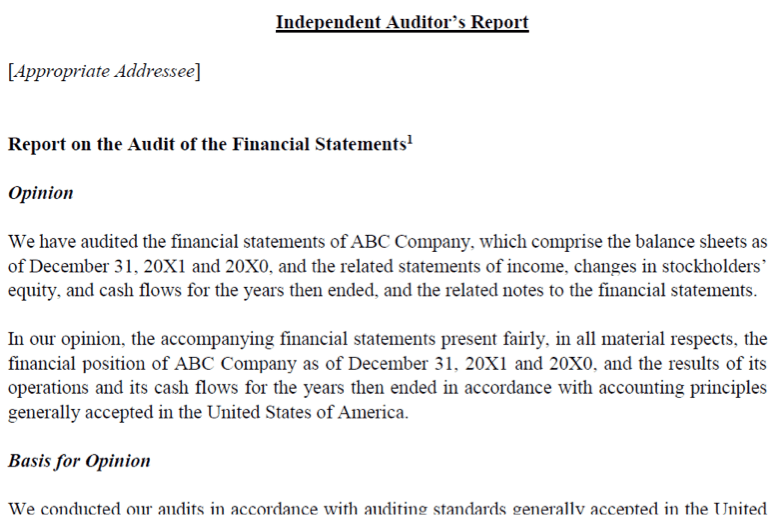

1. Layout

When this standard is adopted, you will notice that the entire layout of the auditor’s report will change from what you are used to. This revised audit report will start with the audit opinion, which is viewed by some as the most important portion of the auditor’s report and was historically reported much later in the auditor’s report, sometimes even the last paragraph.

Below is an example of how the beginning portion of the auditor’s report will look:

The audit opinion will be followed by a “Basis for Opinion” paragraph. This “Basis of Opinion” paragraph is now required in all auditor reports, where it was previously only required in auditor reports with modified opinions.

The purpose of this “Basis for Opinion” paragraph is to set users’ expectations for the auditor’s report. It will include the following:

- The fact that the auditor is required to be independent of the entity and to meet other ethical responsibilities.

- Reference to the section of the auditor’s report that describes the auditor’s responsibilities under GAAS.

- A statement that the audit was conducted in accordance with GAAS in the United States.

- A statement regarding whether the auditor believes the audit evidence obtained during the audit is sufficient and appropriate to provide a basis for the auditor’s opinion.

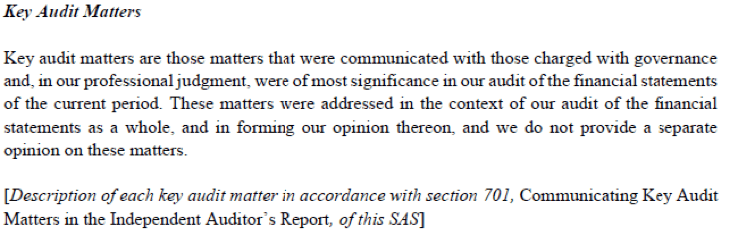

2. Disclosure of key audit matters (KAMs)

Under the new standard, the ASB introduces the optional disclosure of KAMs within the auditor’s report. This allows auditors to communicate significant matters to those charged with governance that are deemed to be the most important or significant to the audit of the financial statements being reported on, as determined by the auditor using professional judgment.

This optional disclosure is comparable to the PCAOB’s standard for public companies requiring the reporting of “critical audit matters” (CAMs) that are discovered during an audit and IAASB standards that instruct auditors on the reporting of “key audit matters.”

Under SAS 134 issued by the ASB, disclosure of KAMs is not required and is only completed by the auditor if the auditor is engaged to do so at the start of the audit engagement by those charged with governance.

So what’s the difference between CAMs and KAMs? Honestly, other than the spelling, not much! The concept of each term is the same — the main difference is the regulatory body that coined each term.

Below is an example of what the KAM section of the auditor’s report may look like for a December 31, 2020, year-end:

While the use of KAMs may not be significant in the private sector for closely-held companies with active ownership, certain users of the financial statements are expected to benefit from these additional disclosures, including private equity firms and not-for-profit entities.

3. Entity’s ability to continue as a going concern

The big news here is that if you do a search for the phrase “going concern” under the new reporting standard, you will get a hit 100% of the time.

This is because one of the requirements of the new expanded “Responsibilities of Management” section specifically states that “Management is required to evaluate, whether there are conditions or events, considered in the aggregate, that raise substantial doubt about the Company’s ability to continue as a going concern ….” This sentence is present whether or not there is actually any doubt about going concern.

Note that this is a big change. Prior to this, the term “going concern” was only present in situations in which it applied.

Additionally, if it is determined by the auditor that substantial doubt exists about an entity’s ability to continue as a going concern, auditors are now required to state this fact in a separate section of the auditor’s report under the following heading: “Substantial Doubt about the Entity’s Ability to Continue as a Going Concern.” This new required paragraph replaces the prior heading entitled “Emphasis-of-Matter,” which was much more vague.

This section is also to be used by the auditor for disclosure of facts and circumstances surrounding going concern if going concern matters relevant to the audit are not appropriately disclosed in the footnotes of the financial statements by management.

4. Additional required statements within the auditor’s report

The new auditor’s report will also include required statements regarding management’s and the auditor’s responsibilities in relation to the audit. These responsibilities are not new concepts to an audit and have always been dictated by GAAS; however, for the first time, they are required to be specifically stated in the auditor’s report.

These matters include:

- Expanded descriptions of the responsibilities of management in relation to the audit, including the evaluation of going concern.

- Expanded descriptions of the responsibilities of the auditor in relation to the audit, including those related to the use of professional judgement and the maintenance of professional skepticism, the evaluation of going concern, and required communication with those in charge of governance.

Are you ready for SAS 134?

Now that you know what the changes are, what do you have to do to prepare for such changes?

You should begin discussions with the users of your financial statements (including banks, shareholders, investors and vendors) related to these changes so that all will understand the meaning behind the new wording when it takes effect.

Also, consider whether the reporting of KAMs would be of interest to the users of your financial statements so that you can appropriately engage your Wipfli auditors when the time comes.

Now is the time to start thinking about these changes so that you and your company and stakeholders can fully benefit from the enhancements the new reporting requirements provide.

If you have any questions about SAS 134 and how it affects your organization, please reach out to us.