Reporting guidance for the SLFRF program

On January 6, 2022, the Treasury adopted the final rule implementing the SLFRF program, with the effective date of April 1, 2022.

On February 28, 2022, the Treasury Department released updated Compliance and Reporting Guidance for the Coronavirus State and Local Fiscal Recovery Funds (SLFRF) program. This guidance is meant to support recipients in complying with the final rule, and provide clarification for each recipient’s compliance and reporting responsibilities under the SLFRF program.

In addition to this guidance, recipients should also follow the award terms and conditions, the authorizing statute, the final rule and other regulatory and statutory requirements, including regulatory requirements under the Uniform Guidance and related Compliance Supplement.

This article will review just the reporting guidance as it relates to the SLFRF, with the compliance guidance to be issued in a separate article.

Reporting guidance

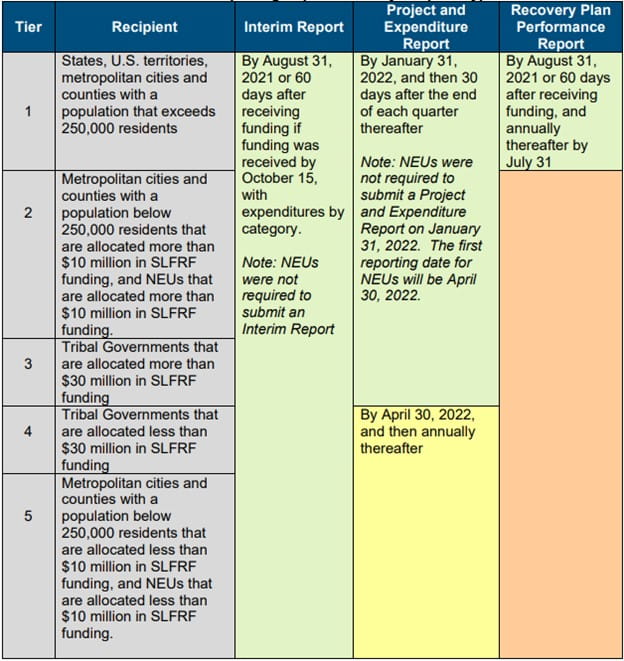

There are three types of reporting requirements for the SLFRF program. The report requirements are approved and documented under OMB PRA number - OMB # 1505-0271.

- Interim report: Provide initial overview of status and uses of funding. This is a one-time report.

- Project and expenditure report: Report on projects funded, expenditures and contracts and subawards over $50,000, and other information.

- Recovery plan performance report: The report will provide information on the projects that large recipients are undertaking with program funding and how they plan to ensure program outcomes are achieved in an effective, efficient and equitable manner. It will include key performance indicators identified by the recipient and some mandatory indicators identified by the Treasury. The recovery plan will be posted on the website of the recipient as well as provided to the Treasury.

The reporting threshold is based on the total award amount allocated by the Treasury under the SLFRF program, not the funds received by the recipient as of the time of reporting.

The following table provided by the Treasury documents the reporting requirements by recipient type:

This updated guidance does not change reporting or compliance requirements pertaining to the Coronavirus Relief Funds (CRF). The following are differences between the CRF and SLFRF programs:

- Project, expenditure and subaward reporting: The SLFRF reporting requirements leverage the existing reporting regime used for CRF to foster continuity and provide many recipients with a familiar reporting mechanism. The data elements for the project and expenditure report will largely mirror those used for CRF, with some minor exceptions noted in this guidance. The users’ guide will describe how reporting for CRF funds will relate to reporting for the SLFRF.

- Timing of reports: CRF reports were due within 10 days of each calendar quarter end. For quarterly reporters, SLFRF reporting will be due the last day of the month following the end of the period covered. For annual reporters, SLFRF reporting will be due on an annual schedule.

- Program and performance reporting: The CRF reporting did not include any program or performance reporting. To build public awareness and accountability and allow the Treasury to monitor compliance with eligible uses, some program and performance reporting is required for SLFRF.

Interim report

Note: The Interim Reports were submitted under the interim final rule.

States, U.S. territories, metropolitan cities, counties and tribal governments were required to submit a one-time interim report with expenditures by expenditure category covering the period from March 3 to July 31, 2021, by August 31, 2021, or 60 days after first receiving funding if the recipient’s date of award was between July 15, 2021, and October 15, 2021. The recipient was required to enter obligations and expenditures and, for each, select the specific expenditure category from the available options.

- Required Programmatic Data Recipients were also required to provide the following information if they had or planned to have expenditures in the following Expenditure Categories.

- Revenue replacement: Key inputs into the revenue replacement formula in the Interim Final Rule and estimated revenue loss due to the COVID-19 public health emergency calculated using the formula in the Interim Final Rule as of December 31, 2020.

- Base year general revenue (e.g., revenue in the last full fiscal year prior to the public health emergency)

- Fiscal year end date

- Growth adjustment used (either 4.1% or average annual general revenue growth over three years prior to pandemic)

- Actual general revenue as of the twelve months ended December 31, 2020

- Estimated revenue loss due to the COVID-19 public health emergency as of December 31, 2020

- An explanation of how revenue replacement funds were allocated to government services

- Revenue replacement: Key inputs into the revenue replacement formula in the Interim Final Rule and estimated revenue loss due to the COVID-19 public health emergency calculated using the formula in the Interim Final Rule as of December 31, 2020.

Project and expenditure report

All recipients are required to submit Project and Expenditure Reports.

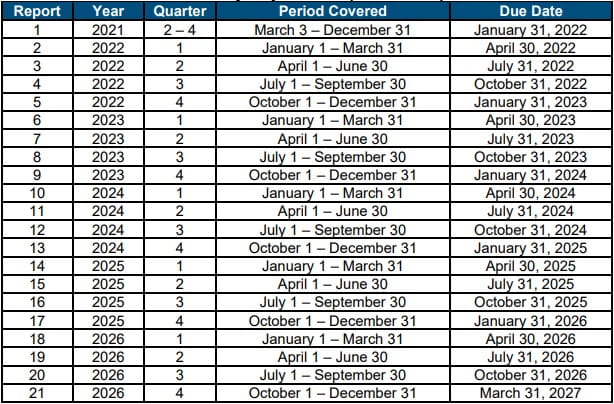

1. Quarterly reporting

The following recipients are required to submit quarterly Project and Expenditure Reports:

- States and U.S. territories

- Tribal governments that are allocated more than $30 million in SLFRF funding

- Metropolitan cities and counties with a population that exceeds 250,000 residents

- Metropolitan cities and counties with a population below 250,000 residents that are allocated more than $10 million in SLFRF funding and NEUs that are allocated more than $10 million in SLFRF funding

For these recipients, the initial quarterly project and expenditure report covers three calendar quarters from March 3, 2021, to December 31, 2021 and was required to be submitted to the Treasury by January 31, 2022. The subsequent quarterly reports will cover one calendar quarter and must be submitted to the Treasury by the last day of the month following the end of the period covered. Quarterly reports are not due concurrently with applicable annual reports. The following table summarizes the quarterly report timelines:

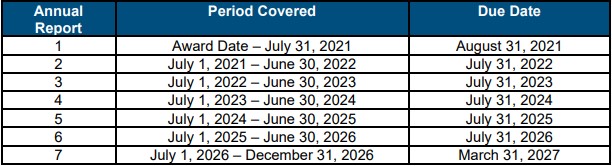

2. Annual reporting

The following recipients are required to submit annual project and expenditure reports:

- Tribal governments that are allocated less than $30 million in SLFRF funding

- Metropolitan cities and counties with a population below 250,000 residents that are allocated less than $10 million in SLFRF funding and NEUs that are allocated less than $10 million in SLFRF funding.

For these recipients, the initial project and expenditure report will cover from March 3, 2021, to March 31, 2022, and must be submitted to the Treasury by April 30, 2022. The subsequent annual reports will cover one calendar year and must be submitted to the Treasury by April 30. The following table summarizes the annual report timelines:

3. Required information

The following information will be required in project and expenditure reports for both quarterly and annual reporting:

- Projects: Provide information on all SLFRF funded projects. For each project, the recipient will be required to enter the project name, identification number (created by the recipient), project expenditure category, description and status of completion. Project descriptions must describe the project in sufficient detail to provide understanding of the major activities that will occur and will be required to be between 50 and 250 words. Projects should be defined to include only closely related activities directed toward a common purpose.

- Obligations and expenditures: Once a project is entered, the recipient will be able to report:

- Current period obligation

- Cumulative obligation

- Current period expenditure

- Cumulative expenditure

- Project status: Once a project in entered, the recipient will be able to report on project status:

- Not Started

- Completed less than 50%

- Completed 50% or more

- Completed

- Program income: Recipients should report any program income earned and expended to cover eligible project costs, if applicable.

- Adopted budget: (States, U.S. territories, metropolitan cities and counties with a population that exceeds 250,000 residents only):

- Each state, territory and metropolitan city and county with a population that exceeds 250,000 residents will provide the budget adopted for each project by its jurisdiction associated with SLFRF funds. The Treasury will use this information to better understand the intended impact, identify opportunities for outreach, and understand the recipient’s progress in program implementation. Treasury is not approving or pre-approving projects or budgets.

- Recipients will enter the adopted budget based on information that exists currently in the recipient’s financial systems and the recipient’s established budget process.

- Each state, territory and metropolitan city and county with a population that exceeds 250,000 residents will provide the budget adopted for each project by its jurisdiction associated with SLFRF funds. The Treasury will use this information to better understand the intended impact, identify opportunities for outreach, and understand the recipient’s progress in program implementation. Treasury is not approving or pre-approving projects or budgets.

- Project demographic distribution:

- Recognizing the disproportionate public health and negative economic impacts of the pandemic on many households, communities and other entities, recipients must report whether certain types of projects are targeted to impacted and disproportionately impacted communities. Recipients will be asked to respond to the following:

- What impacted and/or disproportionally impacted population does this project primarily serve? Please select the population primarily served.

- If this project primarily serves more than one impacted and/or disproportionately impacted population, please select up to two additional populations served.

- Recognizing the disproportionate public health and negative economic impacts of the pandemic on many households, communities and other entities, recipients must report whether certain types of projects are targeted to impacted and disproportionately impacted communities. Recipients will be asked to respond to the following:

- Subawards, contracts, grants, loans, transfers and direct payments: Each recipient shall also provide detailed obligation and expenditure information for any contracts and grants awarded, loans issued, transfers made to other government entities, and direct payments made by the recipient that are greater than $50,000.

- In general, recipients will be asked to provide the following information for each contract, grant, loan, transfer, or direct payment greater than $50,000:

- Subrecipient identifying and demographic information (e.g., DUNS/UEI/TIN number and location)

- Award number (e.g., award number, contract number, loan number)

- Award date, type, amount and description

- Award payment method (reimbursable or lump sum payment(s))

- For loans, expiration date (date when loan expected to be paid in full)

- Primary place of performance

- Related project name(s)

- Related project identification number(s) (created by the recipient)

- Period of performance start date

- Period of performance end date

- Quarterly obligation amount

- Quarterly expenditure amount

- Project(s)

- Additional programmatic performance indicators for select Expenditure Categories

- In general, recipients will be asked to provide the following information for each contract, grant, loan, transfer, or direct payment greater than $50,000:

Aggregate reporting is required for contracts, grants, transfers made to other government entities, loans and direct payments that are below $50,000. This information will be accounted for by expenditure category at the project level. Note that all obligations and expenditures made directly to individuals, regardless of dollar amount, should be included in aggregate reporting.

As required by the 2 CFR Part 170, Appendix A award term regarding reporting subaward and executive compensation, recipients must also report the names and total compensation of their five most highly compensated executives and their subrecipients’ executives for the preceding completed fiscal year if 1) the recipient received 80% or more of its annual gross revenues from Federal procurement contracts (and subcontracts) and Federal financial assistance subject to the Transparency Act, as provided by 2 CFR 170.320 (and subawards), and received $25,000,000 or more in annual gross revenues from Federal procurement contracts (and subcontracts) and Federal financial assistance subject to the Transparency Act (and subawards), and 2) if the information is not otherwise public.

In general, most SLFRF recipients are governmental entities with executive salaries that are already disclosed, so no additional information would be required to be reported. The recipient is responsible for the subrecipients’ compliance with registering and maintaining an updated profile on SAM.gov.

- Civil rights compliance: The Treasury will request information on recipients’ compliance with Title VI of the Civil Rights Act of 1964, as applicable, on an annual basis. This information may include a narrative describing the recipient’s compliance with Title VI, along with other questions and assurances. This collection does not apply to Tribal governments.

- Ineligible activities: Tax offset provision (states and territories only) — The Treasury may collect additional information related to the Tax Offset Provision as described in section 602(c)(2) of the Social Security Act and implemented under 31 CFR 35.8 as part of the Project and Expenditure Report, such as but not limited to revenue reducing covered changes. Please see Section C.11 (Recovery Plan, Ineligible Activities: Tax Offset Provision) for more information.

Recovery plan performance report

Note: The guidance included in this section will be updated prior to July 31, 2022 to align with the final rule. The guidance below, including the Expenditure Categories, reflects the interim final rule.

States, territories, metropolitan cities and counties with a population that exceeds 250,000 residents will also be required to publish and submit to the Treasury a recovery plan performance report. Each recovery plan must be posted on the public-facing website of the recipient by the same date the recipient submits the report to the Treasury. This reporting requirement includes uploading a link to the publicly available document report along with providing data in the Treasury reporting portal.

The recovery plan will provide the public and the Treasury information on the projects recipients are undertaking with program funding and how they are planning to ensure program outcomes are achieved in an effective, efficient and equitable manner.

While this guidance outlines some minimum requirements for the recovery plan, each recipient is encouraged to add information to the plan they feel is appropriate to provide information to their constituents on efforts they are taking to respond to the pandemic and promote economic recovery. Each jurisdiction may determine the general form and content of the recovery plan, as long as it includes the minimum information determined by the Treasury.

The Treasury provided a template (located at www.treasury.gov/SLFRP but recipients may modify this template as appropriate for their jurisdiction. The recovery plan will include key performance indicators identified by the recipient and some mandatory indicators identified by the Treasury.

The initial recovery plan will cover the period from the date of award to July 31, 2021, and must be submitted to the Treasury by August 31, 2021, or 60 days after receiving funding. Thereafter, the recovery plan will cover a 12-month period, and recipients will be required to submit the report to the Treasury within 30 days after the end of the 12-month period (by July 31). The following table summarizes the report timelines:

The recovery plan will include, at a minimum, the following information:

- Executive summary: Provide a high-level overview of the jurisdiction’s intended and actual uses of funding including, but not limited to: the jurisdiction’s plan for use of funds to promote a response to the pandemic and economic recovery, key outcome goals, progress to date on those outcomes and any noteworthy challenges or opportunities identified during the reporting period.

- Uses of funds: Describe in further detail your jurisdiction’s intended and actual uses of the funds, such as how the recipient’s approach would help support a strong and equitable recovery from the COVID-19 pandemic and economic downturn. Describe any strategies employed to maximize programmatic impact and effective, efficient and equitable outcomes. Given the broad eligible uses of funds and the specific needs of the jurisdiction, please also explain how the funds would support the communities, populations or individuals in the recipient’s jurisdiction.

- Promoting equitable outcomes: Describe efforts to promote equitable outcomes, including how programs were designed with equity in mind. Please include in your description how your jurisdiction will consider and measure equity at the various stages of the program.

- Community engagement: Please describe how your jurisdiction’s planned or current use of funds incorporates written, oral, and other forms of input that capture diverse feedback from constituents, community-based organizations and the communities themselves. Where relevant, this description must include how funds will build the capacity of community organizations to serve people with significant barriers to services, including people of color, people with low incomes, limited English proficient populations and other traditionally underserved groups.

- Labor practices: Describe workforce practices on any infrastructure projects being pursued. How are projects using strong labor standards to promote effective and efficient delivery of high-quality infrastructure projects while also supporting the economic recovery through strong employment opportunities for workers? For example, report whether any of the following practices are being utilized: project labor agreements, community benefits agreements, prevailing wage requirements and local hiring.

- Use of evidence: The recovery plan should identify whether SLFRF funds are being used for evidence-based interventions and/or if projects are being evaluated through rigorous program evaluations that are designed to build evidence. Recipients must briefly describe the goals of the project, and the evidence base for the interventions funded by the project. Recipients must specifically identify the dollar amount of the total project spending that is allocated towards evidence-based interventions for each project. Please note that these expenditure categories reflect the interim final rule and will be updated prior to July 31, 2022 to align with the final rule. For all projects, recipients may be selected to participate in a national evaluation, which would study their project along with similar projects in other jurisdictions that are focused on the same set of outcomes. In such cases, recipients may be asked to share information and data that is needed for the national evaluation.

- Table of expenses by expenditure category: Please include a table listing the amount of funds used in each expenditure category. The table should include cumulative expenses to date within each category, and the additional amount spent within each category since the last annual Recovery Plan.

- Project inventory: List the name and provide a brief description of all SLFRF funded projects. Projects are new or existing eligible government services or investments funded in whole or in part by SLFRF funding. For each project, include the project name, funding amount, identification number (created by the recipient and used thereafter in the quarterly program and expenditure report), project expenditure category and a description of the project which includes an overview of the main activities of the project, the approximate timeline, primary delivery mechanisms and partners, if applicable, and intended outcomes.

- Performance report: The recovery plan must include key performance indicators for the major SLFRF funded projects undertaken by the recipient. The recipient has flexibility in terms of how this information is presented in the recovery plan, and may report key performance indicators for each project, or may group projects with substantially similar goals and the same outcome measures.

- Required performance indicators and programmatic data: While recipients have discretion on the full suite of performance indicators to include, a number of mandatory performance indicators and programmatic data must be included. These are necessary to allow the Treasury to conduct oversight as well as understand and aggregate program outcomes across recipients.

- Ineligible activities: Tax Offset Provision (states and territories only) — In each reporting year, states and territories will report certain items related to the Tax Offset Provision as described in section 602(c)(2) of the Social Security Act and implemented by 31 CFR 35.8. Additional guidance will be forthcoming for reporting requirements regarding the tax offset provision and additional information that Recipients will report once the final rule goes into effect.

How Wipfli can help

For those interested in more information regarding the compliance requirements of the SLFRF program, Wipfli regularly performs in-depth trainings on OMB’s Uniform Guidance. Our team is available to help you answer questions or help you navigate and of the complexities of the recovery funds program. Contact us to learn more.

Sign up to receive additional content and information in your inbox, or continue reading: